Tether Minting & Momentum

Tether started as a stable coin with a purported 1:1 backing of USD initially (though at this point we know that Tether is only fractionally backed). It is a defacto fiat currency, with fractional reserves. For better or worse Tether (the company) acts as a central bank of sorts, as appears to have intervened in the market numerous times: for example evidence points to Tether propping up momentum during the 2017 bubble.

Since Tether (USDT) is effectively fiat, new USDT can be minted to buy crypto and prop up the market at little cost to Tether (the company), but at the cost of dilution if the crypto trading is net negative. Note that the evidence for the above is circumstantial but quite compelling, see:

- wikipedia

- 20B$ Scandal

- many other sources and in-depth examinations of the data

Aside from buying (selling) activity that Tether may or may not be doing, given that USDT has the highest cross-pair quoting volume, new investors will need to buy Tether in order to transact with BTC/USDT and other cross pairs. Hence the rate of new Tether (USDT) issuance may be a good indicator of forward momentum (on a longer timeframes).

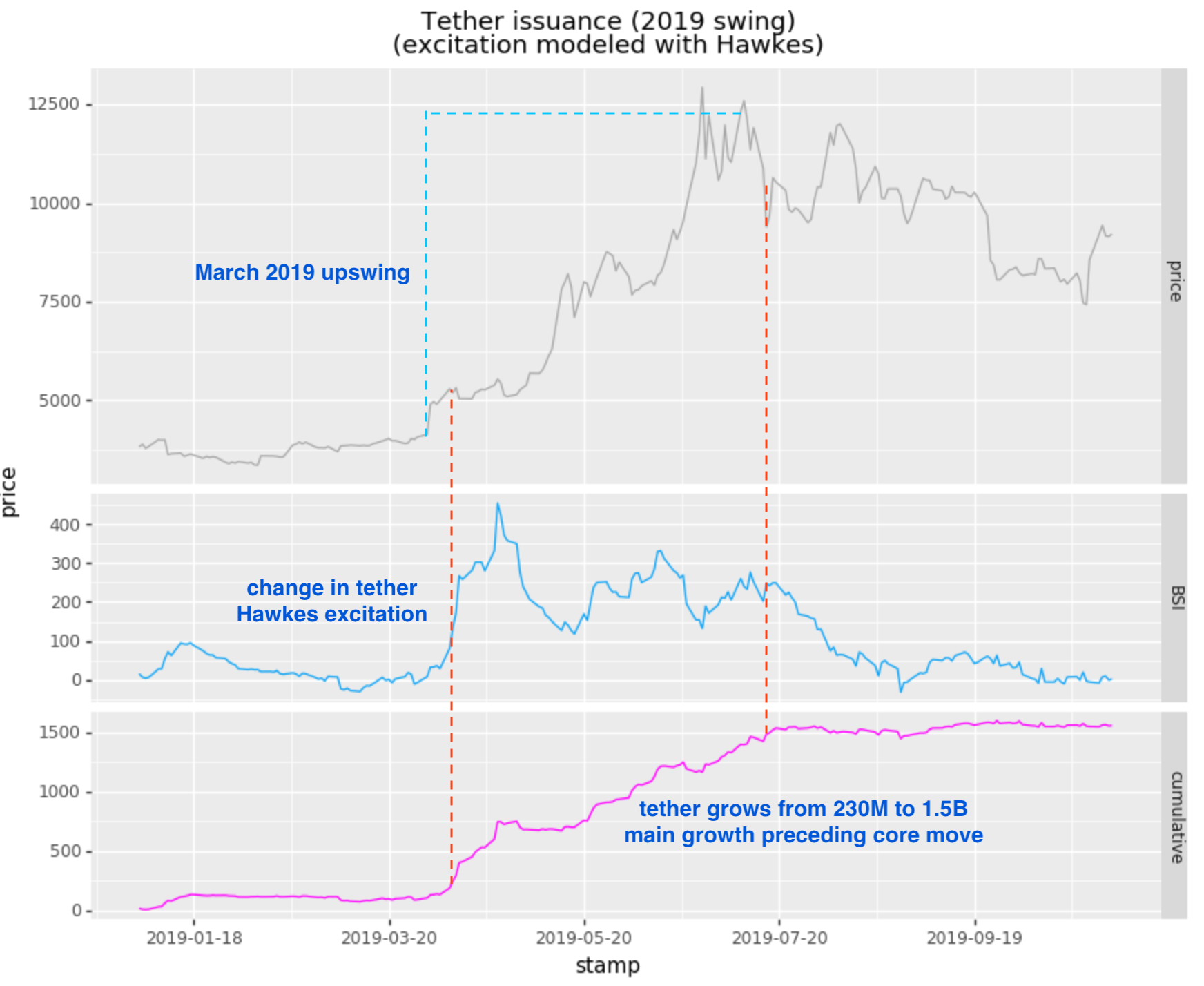

Here is a graph showing spiking new Tether issuance before a market (BTC) move from sub $5000 to $12,500:

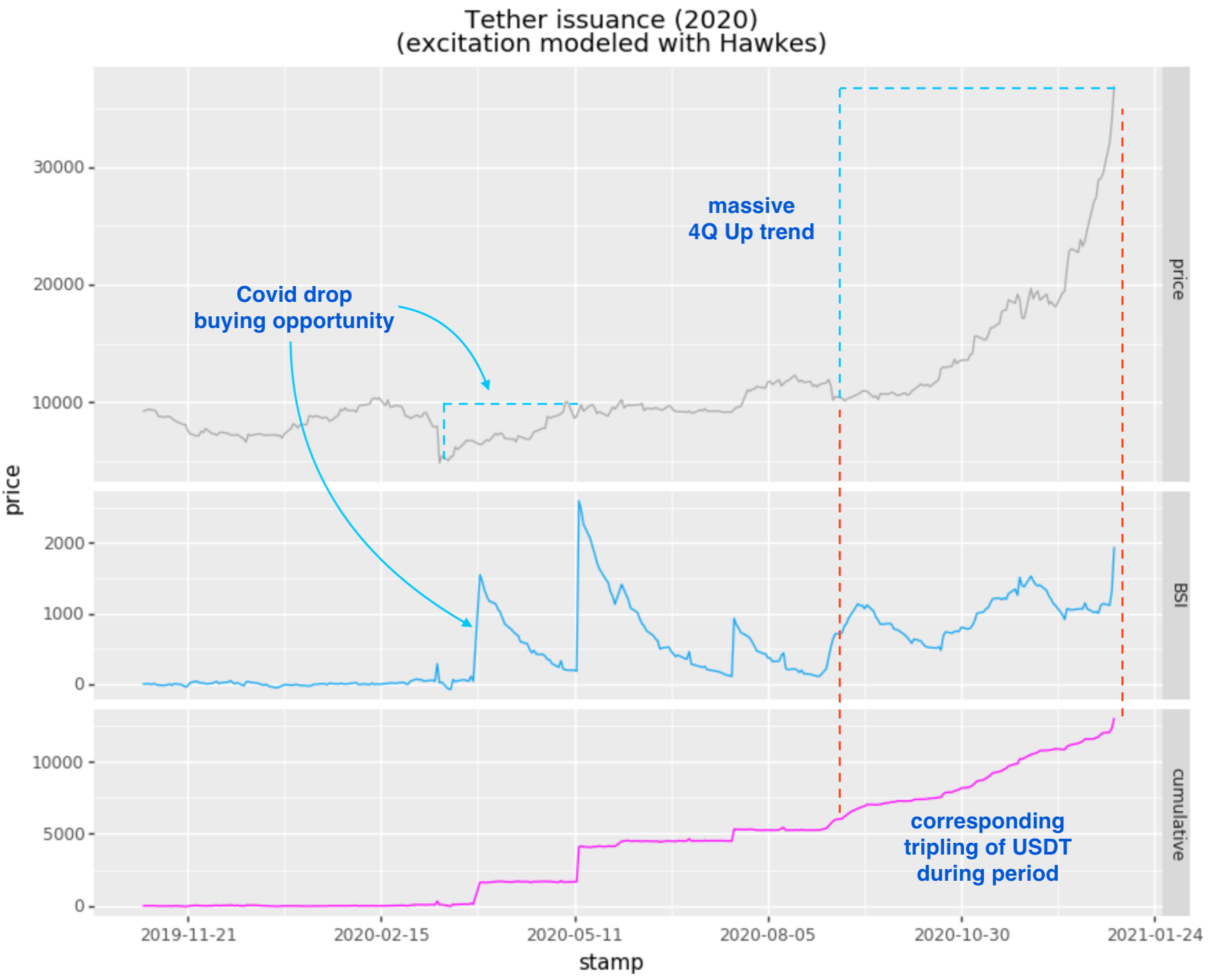

The next graph shows a spike in Tether issuance after the Mar 2020 Covid hiccup, where BTC/USD dropped to $3700 and subsequently regained to the $10,000 mark. Later there is a tripling of issued Tether from Oct to present, corresponding to the massive move from 10K$ to 35K$ (in this period):

We do see a “phantom” spike in Tether buying around 2020-05-11, with no particular forward momentum. Other spikes and/or consistent buying activity to seem to occur before subsequent momentum.

Conclusions

There is definitely a correspondence between Tether issuance spikes and subsequent momentum. For the Q4 trend, the buying is smoother (however massive), so does not spike in the same way. Combining this with other longer-term leading measures, like mempool, should provide an enhanced view of possible forward momentum activity.

I would use this to provide a low-frequency / longer-term view on forward momentum and directional skew. Other higher-freqency indicators, such as BSI (buy/sell imbalance) can provide the local view of momentum.